From The Sacramento Bee (December 20, 2016)

CalPERS moved to slash its official investment forecast Tuesday, a dramatic step that will translate into billions of dollars in higher annual pension contributions from the state, local governments and school districts.

CalPERS’ Finance and Administration Committee voted 6-1 to lower the forecast from 7.5 percent to 7 percent in phases over three years, starting next July. Although the committee’s vote must be ratified by the entire board Wednesday, most other board members indicated they support the move as well.

It would be the first adjustment to the forecast in four years.

The move is a recognition that investment returns are falling and that the California Public Employees’ Retirement System, which is just 68 percent funded, needs higher contributions from government agencies to solve its long-term problems.

“We’re in a low-growth (investment) environment, and it’s expected to remain that way the next five to 10 years,” board member Henry Jones said.

Last week, the investment staff of CalPERS — the $300 billion California pension fund —

Last week, the investment staff of CalPERS — the $300 billion California pension fund —  As consumers and investors, we’re currently confronted by a serious problem: debt. Naturally, because of the global economy,

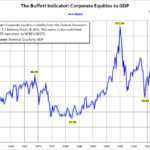

As consumers and investors, we’re currently confronted by a serious problem: debt. Naturally, because of the global economy,  At the beginning of every month, we look at various market valuation metrics to consider forward returns and assess risk levels.

At the beginning of every month, we look at various market valuation metrics to consider forward returns and assess risk levels.